BY TENGKU NOOR SHAMSIAH TENGKU ABDULLAH

SINGAPORE/MANILA, May 4 – ASEAN+3 needs to urgently strengthen cross-border payment connectivity to support regional integration and resilience amid rising global fragmentation and rapid digital transformation, according to a new policy perspectives paper published today by the ASEAN+3 Macroeconomic Research Office (AMRO).

The paper was formally welcomed at the 29th ASEAN+3 Finance Ministers’ and Central Bank Governors’ Meeting held in Manila, where cross-border digital payments were identified as a new area of cooperation under the Updated Strategic Direction of the ASEAN+3 Finance Process underscoring the political weight now attached to the issue.

Authored by a five-member AMRO research team and approved by AMRO leadership, the paper examines the evolving landscape of cross-border payment connectivity across the grouping’s 14 member economies. It notes that globally, cross-border payments remain slow, costly, and opaque problems that persist due to reliance on multiple intermediaries, non-aligned data formats, and legacy infrastructure.

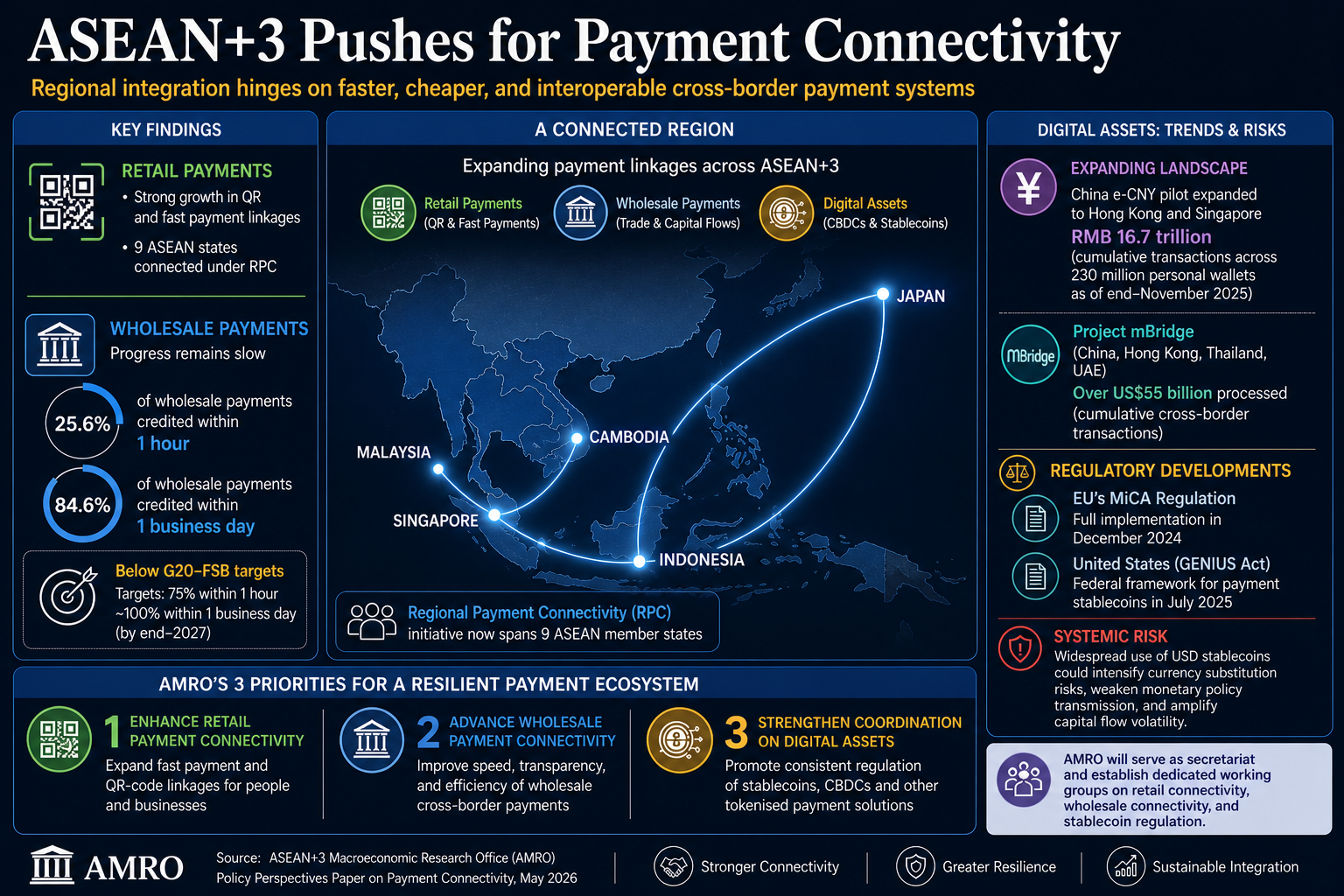

Despite this, ASEAN+3 has emerged as a regional frontrunner in retail payment connectivity. Bilateral linkages built on fast payment systems and QR-code interoperability have expanded significantly since 2020, covering corridors from Malaysia–Singapore to Cambodia–Japan and Indonesia–Japan, with the Regional Payment Connectivity (RPC) initiative now spanning nine ASEAN member states. The region has also made measurable progress on remittance costs, with median costs of sending USD 200 from within ASEAN+3 running nearly 50 basis points below the global average.

Progress in wholesale cross-border payments which underpin trade finance, capital markets activity, and large-value institutional transfers has been considerably slower, however. According to FSB data cited in the paper, only 25.6 percent of wholesale payments in the Asia-Pacific region are credited within one hour of initiation, and 84.6 percent within one business day well below the G20–FSB targets of 75 percent and near-100 percent respectively, set for achievement by end-2027.

The report attributes the lag to structural challenges including fragmented regulatory frameworks, technical disparities across domestic payment systems, stringent AML/CFT compliance requirements for large-value transactions, and shallow local currency foreign exchange markets that limit effective risk management.

The paper is explicit that advancing wholesale connectivity must be a key priority. A holistic approach is needed, it argues one that strengthens not only payment links but also the surrounding ecosystem, including foreign exchange settlement mechanisms, regulatory alignments, liquidity management frameworks, and access to funding.

On digital assets, the study examines the growing but uneven landscape of tokenised payment solutions, including central bank digital currencies (CBDCs) and stablecoins. While these instruments offer potential efficiency gains through instant payments, 24/7 settlement, lower costs, and reduced dependence on correspondent banks, their adoption raises distinct policy risks relating to monetary sovereignty, financial stability, regulatory consistency, and cross-border oversight.

The report maps divergent paths across the region. China’s digital yuan (e-CNY) pilot has expanded to Hong Kong and Singapore, having processed a cumulative RMB 16.7 trillion in transactions across 230 million personal wallets as of end-November 2025. Project mBridge the multi-CBDC platform involving the central banks of China, Hong Kong, Thailand, and the UAE has cumulatively processed over USD 55 billion in cross-border transactions. On the regulatory front, the European Union’s Markets in Crypto-Assets Regulation (MiCA) reached full implementation in December 2024, while the United States passed the GENIUS Act in July 2025, establishing a federal framework for payment stablecoins.

The paper warns that widespread adoption of US dollar-denominated stablecoins could intensify currency substitution risks across the region, weaken domestic monetary policy transmission, and amplify capital flow volatility particularly in economies with less developed regulatory safeguards. It calls for a coordinated ASEAN+3 approach to stablecoin oversight, including supervisory colleges for systemically important stablecoin arrangements and mutual recognition of regulatory frameworks across the region.

More broadly, the AMRO study sets out three interlocking priorities: enhancing retail payment connectivity, advancing wholesale connectivity, and strengthening coordination on digital assets. It stresses that regional initiatives should complement not replace global financial integration, and calls for a multilayered payment ecosystem in which fast payment system linkages, local currency settlement frameworks, stablecoins, and CBDCs can coexist and interoperate effectively.

Given the persistent heterogeneity in legal frameworks, institutions, and technological readiness across member economies, the paper argues that complete regulatory harmonisation is neither feasible nor necessary. Instead, authorities should coordinate to align technical and operational approaches that allow domestic payment systems to interconnect while preserving national autonomy an interoperability-first approach reinforced by strong policy coordination.

AMRO says it is well-positioned to serve as secretariat for sustained regional dialogue and has proposed the establishment of dedicated working groups covering retail payment connectivity, wholesale payment connectivity, and stablecoin regulation.

- TNS NEWS